New Credit Sources

Bitcoins

-

Bitcoin was invented as a peer-to-peer system for online payments that does not require a trusted central authority. Since its inception in 2008, Bitcoin has grown into a technology, a currency, an investment vehicle, and a community of users. In this guide we hope to explain what Bitcoin is and how it works as well as describe how you can use it to improve your life.

What is Bitcoin?

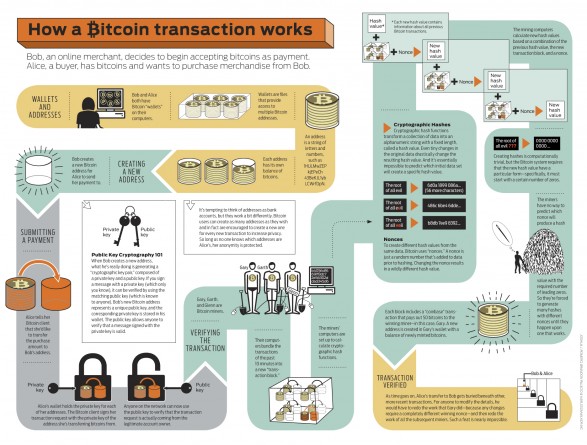

Since anything digital can be copied over and over again, the hard part about implementing a digital payment system is making sure that nobody spends the same money more than once. Traditionally, this is done by having a trusted central authority (like PayPal) that verifies all of the transactions. The core innovation that makes Bitcoin special is that it uses consensus in a massive peer-to-peer network to verify transactions. This results in a system where payments are non-reversible, accounts cannot be frozen, and transaction fees are much lower.

Where do bitcoins come from?

We go more in-depth about this on the page about mining, but here’s a very simple explanation: Some users put their computers to work verifying transactions in the peer-to-peer network mentioned above. These users are rewarded with new bitcoins proportional to the amount of computing power they donate to the network.

Who controls Bitcoin?

As we mentioned above, there is no central person or central authority in charge of Bitcoin. Various programmers donate their time developing the open source Bitcoin software and can make changes subject to the approval of lead developer Gavin Andresen. The individual miners then choose whether to install the new version of the software or stick to the old one, essentially “voting” with their processing power. It is in the miners’ best interest to only accept changes that are good for the Bitcoin currency in the long run. These checks and balances make it difficult for anyone to manipulate Bitcoin.

How Bitcoin Works

-

Long Term - Why Is It Important?

-

Technologies for sharing digitized music had been around for ten years when Fanning came up with Napster. Geeks had been sharing videos for ten years when YouTube came along. Falkvinge thinks Bitcoin will do the same for encrypted e-currency. It’ll do to banking what BitTorrent’s doing to the music industry.

Here’s how Falkvinge describes the ramifications:

“The governments of the world are on the brink of losing the ability to look into the economy of their citizens. They stand to lose the ability to seize assets, they stand to lose the ability to collect debts. … All the world’s weapons in all the world’s police hands are useless against the public’s ability to keep their cryptographic economy to themselves. … The decentralized, uncontrollable economy where one lifetime employment is no longer central to every human being is something I’ve called the swarm economy, and I predict it will redefine society to an immensely larger extent than the ability to get rap music for free.”

This is vitally important to a central theme in my work: The emergence of non-state spaces within which the low-overhead informal and household economy can function, outside the state’s ability to impose artificial scarcities and entry barriers and collect tribute for the usurers, landlords and proprietary content owners.

As Falkvinge argued, it’s usually not the most feature-rich version of a new technology that achieves popular acceptance. Rather, it’s the most user-friendly. “It takes about ten years from conception of a technology, or an application of technology, until somebody hits the magic recipe in how to make that technology easy enough to use that it catches on.”

Bitcoin is monumentally important. Encrypted currency has been at the Altair stage of development. If Bitcoin isn’t actually the Apple II of digital currencies — and it may not be — we’re still just around the corner from that level of popular adoption.

Into The Future

- Neal Stephenson’s cypher-punk sci-fi novel The Diamond Age takes place in a future where encrypted currencies and e-commerce have moved most economic transactions into “darknets” beyond government’s capability of monitoring and regulation, causing tax bases around the world to implode and bringing on the collapse of most nation-states.

Criminals

-

Some of the earliest adopters of the digital currency Bitcoin were criminals, who have found it invaluable in online marketplaces for contraband and as payment extorted through lucrative “ransomware” that holds personal data hostage. A new Bitcoin-inspired technology that some investors believe will be much more useful and powerful may be set to unlock a new wave of criminal innovation.

That technology is known as smart contracts—small computer programs that can do things like execute financial trades or notarize documents in a legal agreement. Intended to take the place of third-party human administrators such as lawyers, which are required in many deals and agreements, they can verify information and hold or use funds using similar cryptography to that which underpins Bitcoin.

Some companies think smart contracts could make financial markets more efficient, or simplify complex transactions such as property deals (see “The Startup Meant to Reinvent What Bitcoin Can Do”). Ari Juels, a cryptographer and professor at the Jacobs Technion-Cornell Institute at Cornell Tech, believes they will also be useful for illegal activity–and, with two collaborators, he has demonstrated how.

“In some ways this is the perfect vehicle for criminal acts, because it’s meant to create trust in situations where otherwise it’s difficult to achieve,” says Juels.

In a paper to be released today, Juels, fellow Cornell professor Elaine Shi, and University of Maryland researcher Ahmed Kosba present several examples of what they call “criminal contracts.” They wrote them to work on the recently launched smart-contract platform Ethereum.

One example is a contract offering a cryptocurrency reward for hacking a particular website. Ethereum’s programming language makes it possible for the contract to control the promised funds. It will release them only to someone who provides proof of having carried out the job, in the form of a cryptographically verifiable string added to the defaced site.

Contracts with a similar design could be used to commission many kinds of crime, say the researchers. Most provocatively, they outline a version designed to arrange the assassination of a public figure. A person wishing to claim the bounty would have to send information such as the time and place of the killing in advance. The contract would pay out after verifying that those details had appeared in several trusted news sources, such as news wires. A similar approach could be used for lesser physical crimes, such as high-profile vandalism.

“It was a bit of a surprise to me that these types of crimes in the physical world could be enabled by a digital system,” says Juels. He and his coauthors say they are trying to publicize the potential for such activity to get technologists and policy makers thinking about how to make sure the positives of smart contracts outweigh the negatives.

“We are optimistic about their beneficial applications, but crime is something that is going to have to be dealt with in an effective way if those benefits are to bear fruit,” says Shi.

Nicolas Christin, an assistant professor at Carnegie Mellon University who has studied criminal uses of Bitcoin, agrees there is potential for smart contracts to be embraced by the underground. “It will not be surprising,” he says. “Fringe businesses tend to be the first adopters of new technologies, because they don’t have anything to lose.”

Indeed, some criminals have made significant gains from Bitcoin. The way it can make digital payments more anonymous has aided the rise of malicious “ransomware” (see “Holding Data Hostage: The Perfect Internet Crime?”). And Christin published a paper this week tracing the evolution of online marketplaces for contraband that have been partly enabled by Bitcoin. It shows that although the most notorious, Silk Road, was taken down by U.S. law enforcement in 2013, others rose in its place and together make sales estimated at around $400,000 a day.

Still, Christin notes that the scale of criminal activity made possible by Bitcoin today, and perhaps by smart contracts in the future, is tiny compared with more traditional, cash-based physical crimes. Smart contracts are also more complex to use than Bitcoin transactions, he adds. Writing a smart contract or properly understanding the terms of one takes specialized programming skills.

Gavin Wood, chief technology officer at Ethereum, notes that legitimate businesses are already planning to make use of his technology—for example, to provide a digitally transferable proof of ownership of gold, and to power a lottery system.

However, Wood acknowledges it is likely that Ethereum will be used in ways that break the law—and even says that is part of what makes the technology interesting. Just as file sharing found widespread unauthorized use and forced changes in the entertainment and tech industries, illicit activity enabled by Ethereum could change the world, he says.

“The potential for Ethereum to alter aspects of society is of significant magnitude,” says Wood. “This is something that would provide a technical basis for all sorts of social changes and I find that exciting.”

For example, Wood says that Ethereum’s software could be used to create a decentralized version of a service such as Uber, connecting people wanting to go somewhere with someone willing to take them, and handling the payments without the need for a company in the middle. Regulators like those harrying Uber in many places around the world would be left with nothing to target. “You can implement any Web service without there being a legal entity behind it,” he says. “The idea of making certain things impossible to legislate against is really interesting.”

Mainstream Banks

-

Bitcoin technology promises to multiply the profitability of investment banks and transform the financial services industry, the heads of Goldman Sachs and UBS have predicted.

The anarchic digital currency has captured the imagination of the banking world. This year Goldman joined a $50 million fundraising for Circle, a bitcoin technology start-up, while last month nine global investment banks teamed up with R3, another fledgeling digital currency business, to devise common standards.

The interest is not in bitcoin itself, but the blockchain technology underpinning it, which enables payments to be processed immediately without an intermediary. For banks, this promises more efficient use of their balance sheets, reduced risk and a freeing up capital to back other opportunities.

At the Institute for International Finance’s annual meeting in Peru, Axel Weber, the chairman of UBS, said that faster settlement times would mean “you can turn over your balance sheet with the same activity 24 times”, rather than only once. “Just imagine the profitability this would bring to financial institutions,” he said. “I see this as a unique opportunity for the banking industry.”

Gary Cohn, Goldman’s chief operating officer, said: “Think of a dollar-yen transaction. I deliver yen in dollars 19 hours later and have that credit exposure sit on my balance sheet, which I have to capitalise. With blockchain technology you settle that in real time simultaneously, free up regulatory capital and everything else. It seems imperative that we get that done.”

There has been an explosion of blockchain start-ups in the past year as technology experts seize an opportunity to disrupt archaic banking systems. The Bank of England has described blockchain as “the first attempt at an internet of finance” and has said that the impact could be “much wider than payments”.

Mr Weber acknowledged the potential threat to traditional banking. “It is true there are many non-banks who drive this. The choice is to innovate or die. We choose to innovate,” he said. UBS has set up a dedicated technology innovation lab in London. For Mr Cohn, blockchain is changing the way that the financial giant thinks of itself. “A third of our people are technologists,” he said. “We are a technology company.”

-

Technologies for sharing digitized music had been around for ten years when Fanning came up with Napster. Geeks had been sharing videos for ten years when YouTube came along. Falkvinge thinks Bitcoin will do the same for encrypted e-currency. It’ll do to banking what BitTorrent’s doing to the music industry.